And if the Federal Government draws the full N4 trillion programme, Nigerians will pay back nearly ₦6.7 trillion — more than the entire debt it was designed to clear

TheDigger Intelligence Unit

The Federal Government has presented its N501.02 billion power sector bond as a landmark intervention — a bold, structured solution to decades of liquidity rot in Nigeria’s electricity market. What it has not presented, at least not in any official communication, is the full bill.

A calculation based on the bond’s published terms — a seven-year tenor, a coupon rate of 16.75% to 17%, and an amortising repayment structure — shows that Nigeria will pay back not N501 billion but N839 billion before the bond matures. Of that, N338 billion is pure interest — money that goes not to fixing a single turbine, laying a single gas pipeline, or lighting a single home, but to servicing the cost of borrowing.

That is 67 kobo in interest for every naira borrowed.

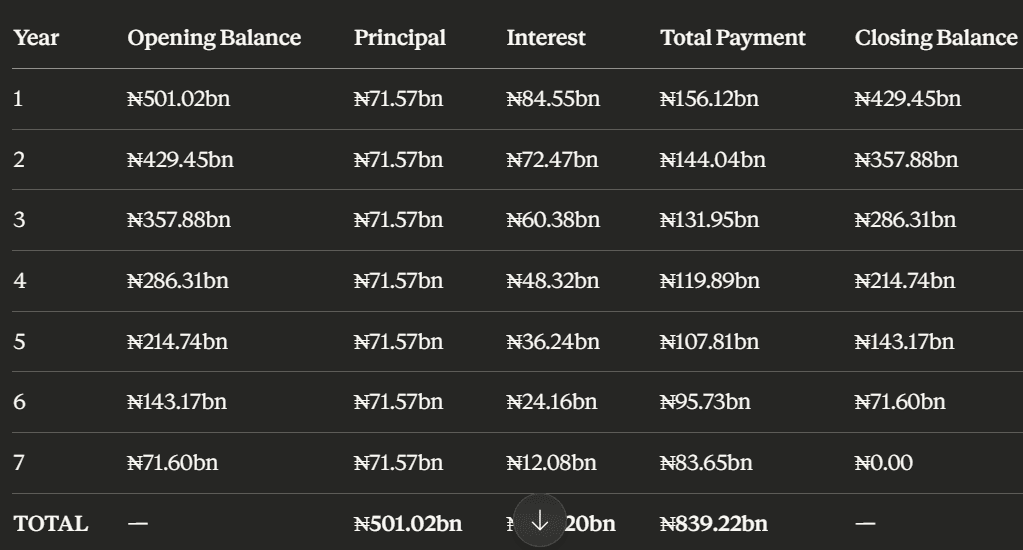

THE REAL COST OF NIGERIA’S N501BN POWER BOND

Assumptions: N501.02bn principal | 16.875% midpoint coupon | 7-year tenor | Equal annual principal amortisation | Interest on declining balance

How The Numbers Break Down

The bond, issued through NBET Finance Company Plc — a Special Purpose Vehicle created by the Nigerian Bulk Electricity Trading Company — carries a fixed coupon at a midpoint rate of 16.875%, paid semi-annually in arrears, with principal repaid in equal annual instalments over seven years.

Under this structure, the repayment burden is heaviest in the early years. In Year 1 alone, the Federal Government will pay N156.12 billion — N71.57 billion in principal and N84.55 billion in interest. By Year 7, as the outstanding balance shrinks, the annual payment falls to N83.65 billion, of which only N12.08 billion is interest.

The cumulative picture is unambiguous: a N501 billion debt obligation becomes an N839 billion fiscal commitment.

The Full Programme — A Far Larger Exposure

The N501 billion Series 1 issuance is only the opening tranche of a much larger exercise. The Federal Executive Council, at its meeting of August 13, 2025, approved a Presidential Power Sector Debt Reduction Programme with a total ceiling of N4 trillion — all of it sovereign-guaranteed, all of it backed by the full faith and credit of the Federal Government of Nigeria.

Phase 1 alone covers N1.23 trillion. If the entire N4 trillion programme is eventually drawn at comparable coupon rates, the interest burden scales accordingly. Under the same 16.875% midpoint rate and amortising structure, the total repayment obligation across the full programme would approach N6.7 trillion — a figure that exceeds the entire N6 trillion-plus debt the programme was designed to eliminate.

In other words, Nigeria risks paying more to clear its power sector debt than the debt itself is worth.

Who Is On The Hook ?

The bond’s primary repayment source is the national budget — meaning Nigerian taxpayers are the ultimate guarantors of every kobo of the N839 billion. A secondary repayment stream relies on NBET recovering revenues from electricity Distribution Companies, a mechanism that has historically proven unreliable. DisCos have been the chronic weak link in the electricity value chain, consistently under-remitting to NBET due to metering gaps, energy theft, and weak billing systems.

If DisCo remittances underperform — as they have for most of the past decade — the full repayment burden reverts to the Federation Account.

Compounding the concern is the question of who holds the bond. The bond achieved 100% subscription by pension funds, banks, and asset managers, but the government has not disclosed the names of these subscribing institutions. As a result, Nigerian workers whose pension savings are invested in this bond have not been informed that their retirement funds are exposed to its risks and returns.

What The Government Has Not Said

Official communications from the Ministry of Power and the Presidential Energy adviser have been consistent in framing the bond in terms of its benefits — restored liquidity, renewed investor confidence, and cleared legacy debts. They have been notably silent on the cost of capital.

No official statement has published a repayment schedule. No press release has disclosed the total interest obligation. The government’s dedicated programme website, energyreforms.ng, details the bond’s credit enhancements, its sovereign guarantee, and its dual listing on the NGX and FMDQ — but contains no amortisation table, no total cost disclosure, and no taxpayer impact assessment.

The N338 billion interest burden is not a secret. It is an arithmetic consequence of publicly available terms. It has simply not been reported.

The Broader Question

None of this is to say the bond is without merit. The power sector’s N6 trillion debt crisis is real, structural, and damaging. Generation companies have been starved of cash. Gas suppliers have been unable to invest. The electricity value chain has been trapped in a vicious cycle of under-recovery that no amount of incremental intervention has broken.

A structured, sovereign-backed, capital market instrument is a more defensible solution than drawing directly from the Federation Account or accumulating further arrears. The bond’s architects are not wrong that something had to be done.

But Nigerians deserve to know the full cost of what is being done in their name. A government that borrows N501 billion and repays N839 billion is not simply clearing a debt — it is creating a new and larger one. And a programme designed to eliminate N6 trillion in sector liabilities, if fully drawn, risks generating nearly N7 trillion in repayment obligations.

Nigerians deserve full transparency and accountability. Demand that the government clearly disclose the total cost and taxpayer impact of these bonds before further commitments are made. Insist on responsible borrowing—one where costs and benefits to the public are fully revealed before the switch is flipped.