Two regulatory violations. A concealed ₦40 billion private placement. Mandatory divestments of foreign subsidiaries. And withheld dividends for shareholders who earned them. TheDiggerNews.com investigates what investors call ‘the left unsaid.’ KEHINDE ADEGOKE uncovers.

In the history of Nigerian banking, no institution has ever posted a ₦1 trillion profit and simultaneously failed to pay its shareholders a single naira in dividends.

Access Holdings Plc achieved both in 2025.

The ₦1.01 trillion pre-tax profit—a record for a Nigerian financial institution—was celebrated. In contrast, the dividend suspension was justified with investor relations jargon: “prudential compliance alignment matters,” “balance sheet actions,” “capital optimisation initiatives.”

Since the May 5, 2026, investor call, TheDiggerNews.com has asked the questions that language was designed to avoid.

These unanswered questions reveal more than a temporary dividend pause: the Group breached two regulatory laws, conducted a secretive ₦40 billion private placement, faces a compelled sell-off of undisclosed assets, and provides an incomplete regulatory picture for shareholders and regulators.

The Soft Language and What It Conceals

Access Holdings selects its words deliberately: “prudential regulatory coordination matters,” “additional matter arose,” “remediate this position.”

What occurred is more exact — and more severe.

In mid-2025, Access Holdings breached Section 7.1 of the CBN Guidelines for Financial Holding Companies, which governs permissible activities, capital, and intergroup exposures. This breach meant the Group operated outside approved parameters when recommending dividends.

At year-end, a more serious breach occurred: Access Holdings’ exposure under BOFIA Section 19(8)(c) reached about 19.3%, nearly double the 10% limit for foreign bank subsidiary investments.

Not a minor misalignment. Not a technical deviation. Almost double the legal limit.

This is not “prudential regulatory coordination.” It is a structural overextension of the parent balance sheet to fund international expansion—a capital management breakdown that the Group’s chosen language aims to obscure.

The ₦40 Billion Private Placement Nobody Scrutinised

Access Holdings says it resolved the half-year breach through a private placement. Management confirmed during the investor call that Access Holdings completed a ₦40 billion private placement, which is part of broader recapitalisation and capital optimisation efforts.

The ₦40 billion private placement, confirmed during the investor call, was a major market event and led to shareholder dilution. NGX and SEC rules require prompt, full disclosure.

TheDiggerNews.com‘s right-of-reply letter to Access Holdings—sent May 10, 2026, with a midnight May 13 deadline—asked six questions about the placement: total size, conclusion date, subscriber identities, price per share, whether it was at a market discount, and whether it was separately announced to the NGX and SEC.

Access Holdings has declined to answer any of them.

The Nigerian Exchange Group and the Securities and Exchange Commission, both recipients of Access Holdings, have declined to answer any of them. They have also remained silent.

Who invested ₦40 billion? On what terms, and did it dilute existing shareholders or involve related parties? The investing public remains uninformed, and responsible institutions are silent.

The Board That Recommended What It Could Not Deliver

Access Holdings confirmed that dividend recommendations were made at both the half-year and full-year stages in 2025, but approvals were withheld due to separate regulatory considerations.

This confirmation raises the core corporate governance question of the investigation—a question TheDiggerNews.com asked Access Holdings in its right-of-reply letter, still unanswered:

At the time the Board recommended each dividend, had management already identified the regulatory limitations?

If yes, the Board of Directors of Access Holdings Plc formally recommended dividend distributions to its shareholders with the knowledge that regulatory approval for those distributions would not be forthcoming. That is a governance failure of the first order. It is the functional equivalent of a company recommending a bonus to employees it cannot pay, without telling them the payment is contingent on an approval it does not have.

If not, management permitted the Board’s formal recommendation to proceed without confirming that the necessary regulatory clearances had been secured. This represents a distinct governance failure—one rooted in inadequate regulatory oversight and in management’s Board reporting.

Both scenarios demand a public explanation. Access Holdings has offered neither.

19.3% vs 10%: The Scale of the Breach in Naira

Access Holdings must now select subsidiaries for stake reduction, secure buyers at proper valuations, and close these transactions in 12 months—across a 24-country network.

By December 31, 2025, the Group’s shareholders’ funds totalled about ₦3.08 trillion. At a 10% threshold, it may invest up to ₦308 billion in foreign subsidiaries. Access Holdings’ exposure stands at about ₦594 billion, or 19.3% of shareholders’ funds.

Access Holdings exceeded the BOFIA limit by about ₦286 billion—over a quarter-trillion naira above the legal maximum.

That figure has not appeared in any public report on this story. Access Holdings has not revealed it. It has not been computed or published by any financial journalist in Nigeria. Its absence keeps the extent of regulatory breach hidden from investors.

TheDiggerNews.com is publishing it now.

The Compelled Sell-Off — and the Questions It Raises

The Group stated it will partially divest from some banking subsidiaries while retaining its super-majority shareholding.

This single sentence—largely ignored by reports—deserves far more scrutiny.

Access Holdings built its 24-country network over decades of planned expansion. Access Bank UK. Access Bank France. Access Bank Rwanda. Access Bank Kenya. Access Bank Ghana. These are not footnotes — they are the foundation of the Group’s pan-African and global ambitions.

Now, the Group is compelled to divest stakes in some subsidiaries—not by preference, but because it expanded beyond what its capital base can lawfully support under Nigerian regulations.

Which subsidiaries, at what valuation, and to whom? Will related parties be buyers? Will the proceeds go to the holding company or remain with the subsidiary? Is this a strategic move or a CBN forbearance condition?

Access Holdings, the CBN, the NGX, and the SEC have not answered any of these questions, despite receiving TheDiggerNews.com’s right-of-reply letter.

The Profit That May Not Be What It Appears

Access Holdings reported gross earnings of ₦5.53 trillion and profit before tax of ₦1.01 trillion for 2025. These are extraordinary figures — historic milestones for Nigerian banking.

A core question remains: how much of the ₦1.01 trillion profit was non-cash foreign exchange translation gains, inflated by naira depreciation in 2024 and 2025?

The bank’s impairment charges more than doubled to ₦523.6 billion in 2025, mainly due to exit from CBN forbearance exposures. This, alongside the BOFIA breach, raises a key question: If Access Holdings claims a strong capital position, how does a company with a 20.2% capital adequacy ratio breach the investment cap by nearly double?

Either the capital base is weaker than presented when adjusted for the foreign subsidiary overexposure, or the foreign subsidiary exposure is dramatically larger than the headline numbers suggest. Both possibilities require a public explanation, as investor trust depends on transparency.

TheDiggerNews.com asked Access Holdings for a breakdown of its 2025 profit between FX gains and core banking income. Access Holdings has not responded.

The Institutions That Should Be Asking These Questions

TheDiggerNews.com formally wrote four institutions before publication—Access Holdings, CBN, SEC, and NGX. Each received specific questions and a May 13 midnight deadline.

None has responded.

That collective silence is itself a finding. Access Holdings, the CBN, SEC, and NGX have not disclosed the terms of the forbearance arrangement, dividend recommendations, or the ₦40 billion private placement, despite TheDiggerNews.com’s specific questions.

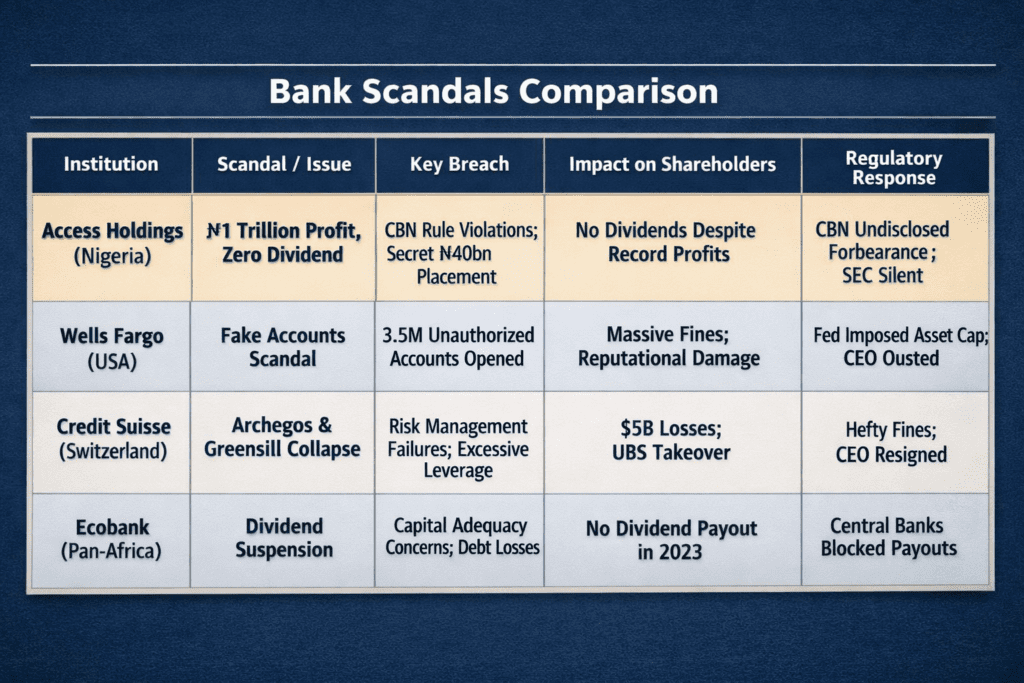

Access Holdings’ dividend suspension mirrors scandals where reported profits were overshadowed by governance and compliance failures. Examples include Wells Fargo’s fake accounts scandal in the U.S., Credit Suisse’s Archegos-linked collapse in Switzerland, and Ecobank’s dividend halt in Africa. Each case shows how regulatory breaches, opaque disclosures, and weak oversight erode investor confidence.

Key Similarities

Regulatory Breaches: All cases involve violations of prudential rules (Access Holdings overexposure, Wells Fargo consumer protection, Credit Suisse risk management, Ecobank capital adequacy).

Shareholder/Customer Harm: Profits or growth were reported, but stakeholders bore losses—either through denied dividends, reputational damage, or direct financial harm.

Opaque Disclosures: Each institution failed to provide timely, transparent information (Access Holdings’ private placement, Wells Fargo’s ignored whistleblowers, Credit Suisse’s hidden leverage, Ecobank’s delayed communication).

Regulatory Silence or Delay: Authorities often acted late or remained silent, amplifying distrust.

Risks & Lessons

Access Holdings resembles Credit Suisse most closely: both have overstretched balance sheets with international exposures, concealed risks, and faced forced restructuring.

Wells Fargo shows the danger of governance culture: Access Holdings’ board recommending dividends it couldn’t deliver echoes Wells Fargo’s leadership failures.

Ecobank illustrates regional parallels: dividend suspension is framed as prudent, but investors still question whether regulatory capital requirements mask deeper weaknesses.

Takeaway

Access Holdings’ case is not isolated—it fits a global pattern where headline profits mask governance failures. The Nigerian situation is particularly alarming because it combines record profitability with zero shareholder reward, regulatory breaches, and silence from oversight bodies. This places it closer to systemic crises like Credit Suisse than to “ordinary” dividend holidays like Ecobank.

Potential Consequences for Access Holdings (Drawing Parallels to Wells Fargo, Credit Suisse, and Ecobank)

If regulators decide to impose stricter penalties on Access Holdings, the fallout could mirror that of other global scandals. Here’s how:

What Must Now Happen

This investigation has identified five specific accountability demands — every one a matter of public record that no institution has yet addressed:

One — Access Holdings must publicly disclose the full terms of the ₦40 billion private placement: subscriber identity, price per share, discount to market, NGX and SEC notification status, and whether related parties were among the subscribers.

Two — Access Holdings must publicly answer whether its Board recommended dividends at half-year and full-year 2025 with knowledge of the outstanding regulatory limitations, and if so, what market disclosures were made at the time of each recommendation.

Three — The CBN must publicly disclose the terms, conditions, reporting obligations, and consequences of the forbearance arrangement granted to Access Holdings under BOFIA Section 19(8)(c) — including whether those terms constitute information that shareholders and the market are entitled to know.

Four — Access Holdings must identify which subsidiaries are under consideration for partial divestment, at what valuation, to whom, and on what timeline — information that is directly material to the value of shareholders’ investments.

Five — The SEC and NGX must publicly confirm whether Access Holdings’ market disclosures in 2025 complied with their respective rules on material disclosure, and, if not, what action is being taken.

The Dig

₦1 trillion in profit. Zero in dividends. Two regulatory breaches. A ₦40 billion private placement with unnamed subscribers. A compelled sell-off across 24 countries. A CBN forbearance arrangement on undisclosed terms. And four regulatory institutions that received formal questions from this publication and chose silence over transparency.

That is not a dividend story. That is a capital management and compliance oversight crisis dressed within investor relations language — and it belongs in the public domain.

Access Holdings’ shareholders — hundreds of thousands of Nigerians who invested in one of the country’s most celebrated financial institutions — earned that dividend. They were told they could not have it. They deserve to know exactly why.

TheDiggerNews.com will continue to pursue this investigation until all five accountability demands are publicly met.

TheDiggerNews.com formally wrote to Access Holdings Plc, the Central Bank of Nigeria, the Securities and Exchange Commission of Nigeria, and the Nigerian Exchange Group on May 10, 2026, with a midnight May 13, 2026, deadline for responses. No response has been received from any of the four institutions as of the date of this publication. Responses will be published in full upon receipt. This investigation is ongoing.

𝗞𝗲𝗵𝗶𝗻𝗱𝗲 𝗔𝗱𝗲𝗴𝗼𝗸𝗲 𝗶𝘀 𝗮𝗻 𝗮𝘄𝗮𝗿𝗱-𝘄𝗶𝗻𝗻𝗶𝗻𝗴 𝗶𝗻𝘃𝗲𝘀𝘁𝗶𝗴𝗮𝘁𝗶𝘃𝗲 𝗷𝗼𝘂𝗿𝗻𝗮𝗹𝗶𝘀𝘁 𝘄𝗶𝘁𝗵 𝗺𝗼𝗿𝗲 𝘁𝗵𝗮𝗻 𝟭𝟱 𝘆𝗲𝗮𝗿𝘀 𝗼𝗳 𝗱𝗶𝘀𝘁𝗶𝗻𝗴𝘂𝗶𝘀𝗵𝗲𝗱 𝗲𝘅𝗽𝗲𝗿𝗶𝗲𝗻𝗰𝗲 𝘂𝗻𝗰𝗼𝘃𝗲𝗿𝗶𝗻𝗴 𝘀𝘁𝗼𝗿𝗶𝗲𝘀 𝘁𝗵𝗮𝘁 𝘀𝗵𝗮𝗽𝗲 𝗽𝘂𝗯𝗹𝗶𝗰 𝗱𝗶𝘀𝗰𝗼𝘂𝗿𝘀𝗲. 𝗪𝗶𝘁𝗵 𝘁𝗵𝗿𝗲𝗲 𝗶𝗻𝗱𝘂𝘀𝘁𝗿𝘆 𝗻𝗼𝗺𝗶𝗻𝗮𝘁𝗶𝗼𝗻𝘀 𝗮𝗰𝗿𝗼𝘀𝘀 𝗱𝗶𝘃𝗲𝗿𝘀𝗲 𝗯𝗲𝗮𝘁𝘀, 𝗵𝗲 𝗵𝗮𝘀 𝗲𝗮𝗿𝗻𝗲𝗱 𝗿𝗲𝗰𝗼𝗴𝗻𝗶𝘁𝗶𝗼𝗻 𝗳𝗼𝗿 𝗳𝗲𝗮𝗿𝗹𝗲𝘀𝘀 𝗿𝗲𝗽𝗼𝗿𝘁𝗶𝗻𝗴, 𝗶𝗻𝗰𝗶𝘀𝗶𝘃𝗲 𝗮𝗻𝗮𝗹𝘆𝘀𝗶𝘀, 𝗮𝗻𝗱 𝗮 𝗰𝗼𝗺𝗺𝗶𝘁𝗺𝗲𝗻𝘁 𝘁𝗼 𝗮𝗰𝗰𝗼𝘂𝗻𝘁𝗮𝗯𝗶𝗹𝗶𝘁𝘆. 𝗔𝘀 𝗠𝗮𝗻𝗮𝗴𝗶𝗻𝗴 𝗘𝗱𝗶𝘁𝗼𝗿 𝗮𝗻𝗱 𝗖𝗘𝗢 𝗼𝗳 𝗧𝗵𝗲𝗗𝗶𝗴𝗴𝗲𝗿𝗡𝗲𝘄𝘀.𝗰𝗼𝗺, 𝗔𝗱𝗲𝗴𝗼𝗸𝗲 𝗹𝗲𝗮𝗱𝘀 𝗮 𝗽𝗶𝗼𝗻𝗲𝗲𝗿𝗶𝗻𝗴 𝗻𝗲𝘄𝘀𝗿𝗼𝗼𝗺 𝗱𝗲𝗱𝗶𝗰𝗮𝘁𝗲𝗱 𝘁𝗼 𝗲𝘅𝗽𝗼𝘀𝗶𝗻𝗴 𝗵𝗶𝗱𝗱𝗲𝗻 𝘁𝗿𝘂𝘁𝗵𝘀, 𝗮𝗺𝗽𝗹𝗶𝗳𝘆𝗶𝗻𝗴 𝗺𝗮𝗿𝗴𝗶𝗻𝗮𝗹𝗶𝘇𝗲𝗱 𝘃𝗼𝗶𝗰𝗲𝘀, 𝗮𝗻𝗱 𝘀𝗲𝘁𝘁𝗶𝗻𝗴 𝗻𝗲𝘄 𝘀𝘁𝗮𝗻𝗱𝗮𝗿𝗱𝘀 𝗶𝗻 𝗶𝗻𝘃𝗲𝘀𝘁𝗶𝗴𝗮𝘁𝗶𝘃𝗲 𝗷𝗼𝘂𝗿𝗻𝗮𝗹𝗶𝘀𝗺.

TheDiggerNews.com | www.thediggernews.com | 08039135472 | Ibadan, Nigeria